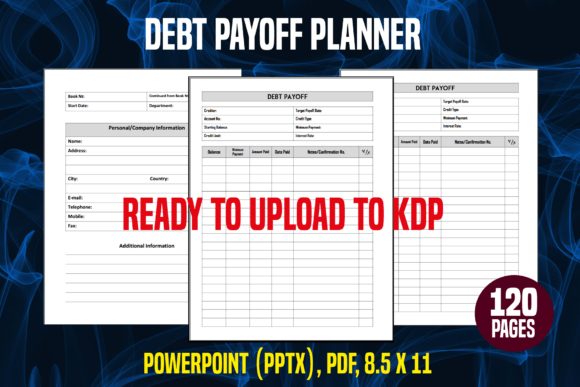

Debt Payoff Planner: A Comprehensive Guide to Financial Freedom

In today’s fast-paced world, managing personal finances can be overwhelming, especially when dealing with debt. Whether you’re struggling with credit card balances, student loans, or other financial obligations, having a clear plan is essential. This is where a Debt Payoff Planner comes into play. A well-structured debt payoff planner helps individuals take control of their finances, reduce stress, and work toward a debt-free future. In this article, we’ll explore what a debt payoff planner is, why it matters, and how you can use it effectively.

What Is a Debt Payoff Planner?

A debt payoff planner is a tool designed to help individuals organize and manage their debts systematically. It typically includes a list of all outstanding debts, their interest rates, minimum payments, and due dates. The goal is to create a structured plan that allows you to pay off your debts efficiently while minimizing the total amount of interest paid over time.

Many people use debt payoff planners to track progress, set realistic goals, and stay motivated. These planners can be in the form of spreadsheets, mobile apps, or even physical documents. For those who prefer a more tangible approach, a PDF file interior ready for upload to KDP or print can serve as an excellent resource. With 120 pages and a trim size of 8.5 x 11, it offers ample space for detailed planning and customization.

The Purpose and Significance of a Debt Payoff Planner

The primary purpose of a debt payoff planner is to provide clarity and direction when it comes to paying off debt. Without a clear plan, it's easy to feel overwhelmed or stuck in a cycle of minimum payments. A planner helps you break down your financial situation into manageable steps, making it easier to tackle each debt one at a time.

One of the key benefits of using a debt payoff planner is that it encourages financial discipline. By tracking your progress, you can see how much you’ve paid off and how much remains, which can be a powerful motivator. Additionally, a planner helps you avoid common pitfalls, such as taking on new debt while trying to pay off existing ones.

For example, imagine you have multiple credit cards with varying interest rates. Without a plan, you might focus on paying off the card with the smallest balance first, only to end up paying more in interest over time. A debt payoff planner helps you prioritize debts based on factors like interest rates, which can save you money in the long run.

How a Debt Payoff Planner Fits Into Modern Life

In today’s digital age, many people rely on technology to manage their finances. However, there is still value in using a physical or printable planner, especially for those who prefer a hands-on approach. A KDP Interior PDF file provides a professional and organized way to keep track of your financial goals. With high-resolution interior pages, it ensures that your planner looks clean and readable, whether you print it or view it digitally.

Moreover, a debt payoff planner can be integrated into various aspects of daily life. For instance, if you're a student, you can use it to track your student loans and budget accordingly. If you're a working professional, it can help you manage credit card debt while saving for retirement. For entrepreneurs, it can be part of a broader financial strategy to ensure business and personal finances remain separate and manageable.

Practical Relevance of a Debt Payoff Planner

Using a debt payoff planner isn’t just about numbers—it’s also about mindset. It encourages you to think critically about your spending habits and make informed decisions. For example, if you notice that you’re consistently overspending on non-essential items, a planner can help you identify these patterns and adjust your budget accordingly.

Another practical benefit is that a debt payoff planner can be tailored to fit your unique financial situation. Whether you’re aiming to pay off $5,000 in credit card debt or $50,000 in student loans, the planner can be customized to reflect your specific goals and timelines. This flexibility makes it a valuable tool for people at all stages of their financial journey.

Examples of How a Debt Payoff Planner Can Help

Let’s look at a few real-life scenarios to illustrate how a debt payoff planner can make a difference:

- Scenario 1: Sarah has three credit cards with balances of $2,000, $3,500, and $4,000. Using a debt payoff planner, she decides to focus on the card with the highest interest rate first, which helps her save money on interest over time.

- Scenario 2: John is a recent college graduate with student loans totaling $25,000. He uses a debt payoff planner to set monthly payment goals and track his progress, which keeps him motivated and on track to become debt-free within five years.

- Scenario 3: Maria runs a small business and has both personal and business debt. She uses a debt payoff planner to separate her personal and business finances, ensuring that she pays off her personal debts without compromising her business operations.

Common Misconceptions About Debt Payoff Planners

Despite their usefulness, some people may have misconceptions about debt payoff planners. One common assumption is that they are only for people with large amounts of debt. In reality, anyone with any type of debt—whether it’s a small credit card balance or a major mortgage—can benefit from using a planner.

Another misconception is that debt payoff planners are too complicated or time-consuming to use. While some planners may require more effort, many are designed to be simple and user-friendly. For instance, a PDF file interior can be filled out manually or digitally, making it accessible for people of all skill levels.

How to Create or Use a Debt Payoff Planner

If you’re looking to create your own debt payoff planner, start by listing all your debts, including the creditor name, balance, interest rate, and minimum payment. Then, decide on a repayment strategy, such as the avalanche method (prioritizing high-interest debts) or the snowball method (prioritizing small balances first).

For those who prefer a ready-made solution, a KDP ZIP file containing an editable source file PowerPoint (.pptx) and a PDF interior can be an excellent choice. This allows you to customize the planner to suit your needs, whether you want to add more columns, change the layout, or include additional notes.

Conclusion

A debt payoff planner is more than just a financial tool—it’s a pathway to greater financial freedom and peace of mind. By organizing your debts, setting clear goals, and staying focused on your progress, you can take control of your financial future. Whether you choose to use a printable PDF, a digital app, or a custom spreadsheet, the key is to stay consistent and committed to your plan.

With the right tools and mindset, paying off debt is not only possible but also achievable. So, take the first step today and start building a healthier relationship with your finances. Your future self will thank you.